Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

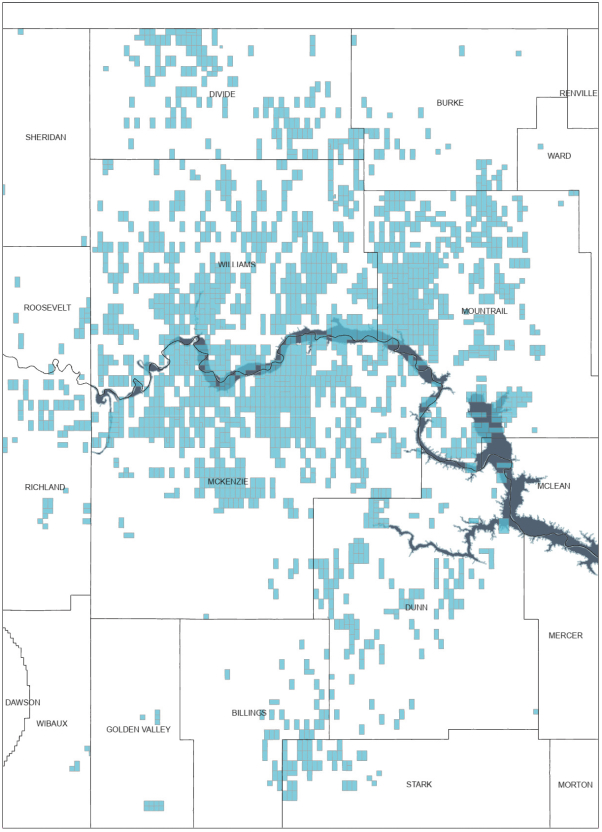

The map below illustrates our acreage position in the Williston Basin as of August 31, 2022.

86

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

Information contained herein is subject to completion or amendment. A Registration Statement on Form 10 relating to these securities has been confidentially submitted with the Securities and Exchange Commission under the Securities Exchange Act of 1934, as amended.

Exhibit 99.1

PRELIMINARY AND SUBJECT TO COMPLETION, DATED OCTOBER 12, 2022

INFORMATION STATEMENT

Vitesse Energy, Inc.

Common Stock

(par value $0.01)

We are sending you this Information Statement in connection with the spin-off by Jefferies Financial Group Inc., which we refer to as “Jefferies,” of its newly formed indirect majority owned subsidiary, Vitesse Energy, Inc., which we refer to as “Vitesse” or “we.” Prior to the spin-off, Vitesse will acquire all of the issued and outstanding equity interests of Vitesse Energy, LLC, which we refer to as “Vitesse Energy,” and Vitesse Oil, LLC, which we refer to as “Vitesse Oil,” which together represent substantially all of those businesses or investments of Jefferies that acquire, develop, manage and monetize non-operated oil and natural gas working, royalty and mineral interests in the United States, primarily in the Bakken and Three Forks formations in the Williston Basin in North Dakota and Montana. Following Vitesse’s acquisitions of Vitesse Energy and Vitesse Oil and a series of transactions described in this Information Statement, Jefferies will hold approximately [ ]% of the total issued and outstanding Vitesse common stock immediately prior to the spin-off. To effect the spin-off, Jefferies will distribute all of the issued and outstanding shares of Vitesse common stock held by Jefferies to the holders of Jefferies common stock on a pro-rata basis. After the distribution, Jefferies will not own any shares of Vitesse common stock. The distribution of Vitesse common stock is intended to be tax-free to Jefferies shareholders for U.S. federal income tax purposes, except for cash that shareholders receive in lieu of fractional shares and subject to the discussion in the section entitled “The Spin-Off—Material U.S. Federal Income Tax Consequences of the Spin-Off—Consequences to Holders of Jefferies Common Stock.” You should consult your own tax advisor as to the tax consequences of the distribution to you, including potential tax consequences under state, local and non-U.S. tax laws.

If you are a record holder of Jefferies common stock as of the close of business on [ ], 2022, which is the record date for the distribution, for every [ ] shares of Jefferies common stock you hold on that date, you will be entitled to receive [ ] shares of Vitesse common stock. Jefferies will distribute the shares of Vitesse common stock in book-entry form, which means that we will not issue physical stock certificates. The distribution agent will not distribute any fractional shares of Vitesse common stock. Instead, the distribution agent will aggregate fractional shares into whole shares, sell the whole shares in the open market at prevailing market prices and distribute the aggregate cash proceeds of the sales, net of brokerage fees and other costs, to each holder pro rata (net of any required withholding for taxes applicable to each holder) in lieu of any fractional share to which the holder otherwise would have been entitled to receive in the distribution. As discussed in the section entitled “The Spin-Off—Trading Prior to the Distribution Date,” if you sell your shares of Jefferies common stock in the “regular-way” market after the record date and on or before the distribution date, you also will be selling your right to receive shares of Vitesse common stock in connection with the distribution.

We expect that the distribution will be effective as of [ ], New York City time, on [ ], 2022. Immediately after the distribution becomes effective, Vitesse will be an independent, publicly traded company.

Jefferies shareholders are not required to vote on or take any other action in connection with the spin-off. We are not asking you for a proxy and you are requested not to send us a proxy. Jefferies shareholders will not be required to pay any consideration for the shares of Vitesse common stock they receive in the spin-off, and they will not be required to surrender or exchange their shares of Jefferies common stock or take any other action in connection with the spin-off.

No trading market for Vitesse common stock currently exists. We expect, however, that a limited trading market for Vitesse common stock, commonly known as a “when-issued” trading market, will develop on the third trading day before the distribution date, and we expect “regular-way” trading of Vitesse common stock will begin on the first trading day after the distribution date. We intend to list Vitesse common stock on the New York Stock Exchange under the ticker symbol “VTS.” Following the distribution, Jefferies will continue to trade on the New York Stock Exchange under the ticker symbol “JEF.”

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012.

In reviewing this Information Statement, you should carefully consider the matters described in the section entitled “Risk Factors” beginning on page 26 of this Information Statement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this Information Statement is truthful or complete. Any representation to the contrary is a criminal offense.

This Information Statement is not an offer to sell, or a solicitation of an offer to buy, any securities.

The date of this Information Statement is [ ], 2022.

This Information Statement was first mailed to Jefferies shareholders on or about [ ], 2022.

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

TABLE OF CONTENTS

| PAGE | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 4 | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 7 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 20 | ||||

| 26 | ||||

| 26 | ||||

| 30 | ||||

| 33 | ||||

| 46 | ||||

| 48 | ||||

| 54 | ||||

| 56 | ||||

| 56 | ||||

| 56 | ||||

| 58 | ||||

| 58 | ||||

| 59 | ||||

| 59 | ||||

| Material U.S. Federal Income Tax Consequences of the Spin-Off |

59 | |||

| 62 | ||||

| 63 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

| 65 | ||||

| 66 | ||||

| 67 | ||||

| 68 | ||||

| 69 | ||||

i

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| PAGE | ||||

| 72 | ||||

| 76 | ||||

| 81 | ||||

| 81 | ||||

| 83 | ||||

| 84 | ||||

| 85 | ||||

| 87 | ||||

| 93 | ||||

| 94 | ||||

| 94 | ||||

| 95 | ||||

| 95 | ||||

| 95 | ||||

| 99 | ||||

| 100 | ||||

| 100 | ||||

| 100 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

101 | |||

| 101 | ||||

| 102 | ||||

| 102 | ||||

| 102 | ||||

| 103 | ||||

| 104 | ||||

| 105 | ||||

| 113 | ||||

| 117 | ||||

| 118 | ||||

| 119 | ||||

| 119 | ||||

| 121 | ||||

| 121 | ||||

| 122 | ||||

| 124 | ||||

| 124 | ||||

| 124 | ||||

| 124 | ||||

| 126 | ||||

| 127 | ||||

| 128 | ||||

| Historical Compensation Paid or Awarded Under Vitesse Energy Plans and Arrangements |

128 | |||

| 128 | ||||

| 128 | ||||

| 129 | ||||

| 129 | ||||

| 129 | ||||

| 130 | ||||

| 130 | ||||

| 130 | ||||

ii

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| PAGE | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

133 | |||

| 133 | ||||

| 134 | ||||

| 135 | ||||

| 135 | ||||

| 136 | ||||

| 136 | ||||

| 137 | ||||

| 137 | ||||

| 137 | ||||

| 138 | ||||

| 138 | ||||

| 138 | ||||

| 138 | ||||

| 139 | ||||

| 139 | ||||

| 140 | ||||

| 141 | ||||

| 141 | ||||

| 141 | ||||

| 148 | ||||

| F-1 | ||||

iii

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

In this Information Statement, unless the context otherwise requires:

| ∎ | “3B Energy” refers to 3B Energy, LLC, the holder of a minority of the equity interests in Vitesse Energy prior to the Pre-Spin-Off Transactions and an entity owned by Bob Gerrity, our Chief Executive Officer and a member of our Board, and Brian Cree, our President and Chief Operating Officer; |

| ∎ | “Amended and Restated Bylaws” refers to the bylaws of Vitesse that will be in effect immediately prior to the Distribution Date; |

| ∎ | “Amended and Restated Certificate of Incorporation” refers to the certificate of incorporation of Vitesse that will be in effect immediately prior to the Distribution Date; |

| ∎ | “AST” refers to American Stock Transfer and Trust Company, LLC; |

| ∎ | “Basin” refers to a large natural depression on the earth’s surface in which sediments generally brought by water accumulate; |

| ∎ | the “Board” refers to our board of directors; |

| ∎ | “Bbl” refers to one stock tank barrel, of 42 U.S. gallons liquid volume, used herein in reference to oil, condensate or NGLs; |

| ∎ | “Boe” refers to barrels of oil equivalent, calculated by converting natural gas to oil equivalent barrels at a ratio of six Mcf of natural gas to one Bbl of oil and at a ratio of one Bbl of NGL to one Bbl of oil; |

| ∎ | “Boe/d” refers to one Boe per day; |

| ∎ | “Btu” refers to a British thermal unit, which is the quantity of heat required to raise the temperature of one pound of water by one degree Fahrenheit; |

| ∎ | “completion” refers to the process of preparing an oil and natural gas wellbore for production through the installation of permanent production equipment, as well as perforation and fracture stimulation to optimize production of oil, natural gas and/or NGLs; |

| ∎ | “condensate” refers to a mixture of hydrocarbons that exists in the gaseous phase at original reservoir temperature and pressure, but that, when produced, is in the liquid phase at surface pressure and temperature; |

| ∎ | “CAA” refers to the Clean Air Act; |

| ∎ | “Cawley” refers to Cawley, Gillespie & Associates, Inc.; |

| ∎ | “CERCLA” refers to the Comprehensive Environmental, Response, Compensation, and Liability Act; |

| ∎ | “CFTC” refers to the Commodities Futures Trading Commission; |

| ∎ | the “Code” refers to the Internal Revenue Code of 1986, as amended; |

| ∎ | “COVID-19” refers to the SARS-CoV-2 novel coronavirus and known variants; |

| ∎ | “CWA” refers to the Federal Water Pollution Control Act of 1972; |

| ∎ | “DGCL” refers to the General Corporation Law of the State of Delaware; |

| ∎ | “Differential” refers to an adjustment to the price of oil or natural gas from an established spot market price to reflect differences in the quality and/or location of oil or natural gas; |

| ∎ | the “Distribution” refers to the transaction in which Jefferies will distribute to its shareholders all outstanding shares of our common stock held by Jefferies; |

| ∎ | the “Distribution Date” refers to the date on which the Distribution occurs; |

| ∎ | the “Dodd-Frank Act” refers to the Dodd-Frank Wall Street Reform and Consumer Protection Act; |

| ∎ | the “DOI” refers to the Department of the Interior; |

| ∎ | “dry hole” refers to a well found to be incapable of producing oil and natural gas in sufficient quantities to justify completion; |

| ∎ | the “EPA” refers to the Environmental Protection Agency; |

| ∎ | the “ESA” refers to the Endangered Species Act; |

| ∎ | “ESG” refers to environmental, social and governance; |

| ∎ | “Exchange Act” refers to the Securities Exchange Act of 1934; |

iv

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| ∎ | “Existing Revolving Credit Facility” refers to Vitesse Energy’s Amended and Restated Credit Agreement, dated as of April 29, 2022, as amended from time to time, among Vitesse Energy, as borrower, Wells Fargo Bank, N.A., as administrative agent, and the lenders party thereto; |

| ∎ | “FERC” refers to the Federal Energy Regulatory Commission; |

| ∎ | “FTC” refers to the Federal Trade Commission; |

| ∎ | “GAAP” refers to accounting principles generally accepted in the United States; |

| ∎ | “Gerrity Bakken” refers to Gerrity Bakken, LLC, the holder of a minority of the equity interests in Vitesse Oil and an entity owned by Bob Gerrity, our Chief Executive Officer and a member of our Board; |

| ∎ | “GHGs” refer to greenhouse gases; |

| ∎ | “gross acres” refers to the total acres in which a working interest is owned; |

| ∎ | “gross wells” refers to the total wells in which a working interest is owned; |

| ∎ | “IPOs” refer to initial public offerings; |

| ∎ | “IRS” refers to the Internal Revenue Service; |

| ∎ | “IRS Ruling” refers to a private letter ruling being sought by Jefferies from the IRS; |

| ∎ | “Jefferies” refers to Jefferies Financial Group Inc. and its consolidated subsidiaries other than, for all periods following the Spin-Off, Vitesse, unless the context requires otherwise; |

| ∎ | “Jefferies Board” refers to Jefferies’ board of directors; |

| ∎ | “Jefferies Capital Partners” refers to Jefferies Capital Partners V L.P. and Jefferies SBI USA Fund L.P., collectively, the holders of a majority of the equity interests in Vitesse Oil and entities in which Jefferies holds an indirect limited partner interest; |

| ∎ | “Jefferies Parties” refers to Jefferies, Jefferies Capital Partners and [ ]; |

| ∎ | “MBbls” refers to one thousand barrels of oil or NGLs; |

| ∎ | “MBoe” refers to one thousand barrels of oil equivalent; |

| ∎ | “Mcf” refers to one thousand cubic feet of natural gas; |

| ∎ | “MMBoe” refers to one million barrels of oil equivalent; |

| ∎ | “MMBtu” refers to one million British thermal units; |

| ∎ | “MMcf” refers to one million cubic feet of natural gas; |

| ∎ | “net acres” refers to the sum of the fractional working interests owned in gross acres (e.g., a 10% working interest in a lease covering 1,280 gross acres is equivalent to 128 net acres); |

| ∎ | “net wells” refers to wells that are deemed to exist when the sum of fractional ownership working interests in gross wells equals one; |

| ∎ | “NEPA” refers to the National Environmental Policy Act; |

| ∎ | “New Revolving Credit Facility” refers to Vitesse’s senior secured revolving credit facility in effect following the completion of the Spin-Off; |

| ∎ | “NGLs” refer to natural gas liquids; |

| ∎ | “NSPS” refers to New Source Performance Standards; |

| ∎ | “NYBCL” refers to the New York Business Corporation Law; |

| ∎ | “NYMEX” refers to the New York Mercantile Exchange; |

| ∎ | “NYSE” refers to the New York Stock Exchange; |

| ∎ | “OPEC” refers to the Organization of Petroleum Exporting Countries; |

| ∎ | “OPA” refers to the Oil Pollution Act of 1990; |

| ∎ | “OTC” refers to the over-the-counter market; |

| ∎ | “PDP” or “proved developed producing” refers to proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods; |

| ∎ | “PDNP” or “proved developed non-producing” refers to proved reserves that are developed behind pipe and are expected to be recovered from zones in existing wells that will require additional completion work or future recompletion prior to the start of production; |

| ∎ | “PHMSA” refers to the Pipeline and Hazardous Materials Safety Administration; |

v

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| ∎ | “possible reserves” refers to the additional reserves which analysis of geoscience and engineering data suggest are less likely to be recoverable than probable reserves; |

| ∎ | “Pre-Spin-Off Transactions” refers to the series of transactions, including Vitesse’s acquisitions of Vitesse Energy and Vitesse Oil, described under “The Spin-Off—Pre-Spin-Off Transactions”; |

| ∎ | “probable reserves” refers to the additional reserves which analysis of geoscience and engineering data indicate are less likely to be recovered than proved reserves but which, together with proved reserves, are as likely as not to be recovered; |

| ∎ | “productive well” refers to a well that is found to be capable of producing oil and natural gas in sufficient quantities such that proceeds from the sale of the production exceed production expenses and taxes; |

| ∎ | “proved developed reserves” refers to proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods or in which the cost of new equipment or operating methods is relatively minor compared to the cost of a new well; |

| ∎ | “proved reserves” refers to the quantities of oil and natural gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible, from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations, prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time; |

| ∎ | “PUD” or “proved undeveloped” refers to proved reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for development. Reserves on undrilled acreage are limited to those drilling units offsetting productive units that are reasonably certain of production when drilled. Undrilled locations can be classified as having undeveloped reserves only if a development plan has been adopted indicating that they are scheduled to be drilled within five years unless specific circumstances justify a longer time. Under no circumstances shall estimates of proved undeveloped reserves be attributable to any acreage for which an application of fluid injection or other improved recovery technique is contemplated, unless such techniques have been proved effective by actual projects in the same reservoir or an analogous reservoir, or by other evidence using reliable technology establishing reasonable certainty: |

| ∎ | “RCRA” refers the Federal Resource Conservation and Recovery Act; |

| ∎ | “Record Date” refers to [ ], 2022; |

| ∎ | “reserves” refers to estimated remaining quantities of oil and gas and related substances anticipated to be economically producible, as of a given date, by application of development projects to known accumulations. In addition, there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil and gas or related substances to market, and all permits and financing required to implement the project; |

| ∎ | “SDWA” refers to the Safe Drinking Water Act; |

| ∎ | “SEC” refers to the Securities and Exchange Commission; |

| ∎ | “Securities Act” refers to Securities Act of 1933; |

| ∎ | “Stockholder Nominee” refers to a candidate for the Board who is nominated by stockholders pursuant to the requirements of our Amended and Restated Bylaws; |

| ∎ | “SOFR” refers to the Secured Overnight Financing Rate; |

| ∎ | the “Spin-Off” refers to our separation from Jefferies and the creation of an independent, publicly traded company, Vitesse, through (1) the Pre-Spin-Off Transactions and (2) the Distribution; |

| ∎ | “Standardized Measure” refers to discounted future net cash flows estimated by applying year-end SEC prices (based on the 12-month unweighted arithmetic average of the first-day-of-the-month oil and natural gas prices for such year-end period) to the estimated future production of year-end proved reserves. Future cash flows are reduced by estimated future production and development costs, including asset retirement obligations, based on year-end costs to determine pre-tax cash inflows. Future income taxes, if applicable, are computed by applying the statutory tax rate to the excess of pre-tax cash flows over our tax basis in the oil and natural gas properties. Future net cash flows after income taxes are discounted using a 10% annual discount rate; |

vi

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| ∎ | “Treasury Regulations” refers to final, temporary, and (to the extent they can be relied upon) proposed regulations under the Code, as promulgated from time to time (including corresponding provisions and succeeding provisions); |

| ∎ | “Two-stream basis” refers to the reporting of production or reserve volumes of oil and wet natural gas, where the NGLs have not been removed from the natural gas stream, and the economic value of the NGLs is included in the wellhead natural gas price; |

| ∎ | “USRPHC” refers to United States real property holding corporation; |

| ∎ | “Vitesse,” “we,” “our” and “us” (1) when used in the past tense, refer to Vitesse Energy and do not give effect to the consummation of the Pre-Spin-Off Transactions, and (2) when used in the present tense or future tense, refer to Vitesse Energy, Inc. and its consolidated subsidiaries and give effect to the consummation of the Pre-Spin-Off Transactions, in each case unless the context requires otherwise; |

| ∎ | “Vitesse Energy” refers to Vitesse Energy, LLC and its consolidated subsidiaries; |

| ∎ | “Vitesse Energy Finance” refers to Vitesse Energy Finance LLC, the holder of a majority of the equity interests in Vitesse Energy prior to the Pre-Spin-Off Transactions and an indirect wholly owned subsidiary of Jefferies; |

| ∎ | “Vitesse Energy MIUs” refers to management incentive units with respect to Vitesse Energy; |

| ∎ | “Vitesse Oil” refers to Vitesse Oil, LLC; |

| ∎ | “Vitesse Oil MIUs” refers to management incentive units with respect to Vitesse Oil; |

| ∎ | “Vitesse Oil Revolving Credit Facility” refers to Vitesse Oil’s Credit Agreement, dated as of July 23, 2015, as amended from time to time, among Vitesse Oil, as borrower, Wells Fargo Bank, N.A., as administrative agent, and the lenders party thereto; |

| ∎ | “VOCs” refers to volatile organic compounds; |

| ∎ | “WOTUS” refers to the waters of the United States; and |

| ∎ | “WTI” refers to West Texas Intermediate. |

vii

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

PRESENTATION OF FINANCIAL AND OPERATING DATA

Unless otherwise indicated, the historical financial information presented in this Information Statement is that of our predecessor, Vitesse Energy. The pro forma condensed combined financial information in this Information Statement is derived from the audited consolidated financial statements and unaudited condensed consolidated financial statements of Vitesse Energy included elsewhere in this Information Statement, which we refer to as the “Audited Consolidated Financial Statements” and the “Unaudited Condensed Consolidated Financial Statements,” respectively. The pro forma condensed combined financial information reflects, among other things, the consummation of the Spin-Off, including the acquisition of Vitesse Oil.

In addition, unless otherwise indicated, the reserve and operational data presented in this Information Statement is with respect to all of the assets of Vitesse Energy prior to giving effect to the Spin-Off.

This Information Statement includes information concerning our industry and the markets in which we operate that is based on information from public filings, internal company sources, various third-party sources and management estimates. Management’s estimates regarding Vitesse’s position, share and industry size are derived from publicly available information and our internal research, and are based on assumptions we made upon reviewing such data and our knowledge of such industry and markets, which we believe to be reasonable. While we are not aware of any misstatements regarding any industry data presented in this Information Statement and believe such data to be accurate, we have not independently verified any data obtained from third-party sources and cannot assure you of the accuracy or completeness of such data. Such data involve uncertainties and are subject to change based on various factors, including those discussed in the section entitled “Risk Factors.”

We own or have rights to various trademarks, logos, service marks and trade names that we use in connection with the operation of our business. We also own or have the rights to copyrights that protect the content of our products. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this Information Statement are listed without the ™, ® or © symbols, but such references do not constitute a waiver of any rights that might be associated with the respective trademarks, service marks, trade names and copyrights included or referred to in this Information Statement.

viii

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

This summary highlights selected information from this Information Statement and provides an overview of our company, our separation from Jefferies and Jefferies’ distribution of our common stock to its shareholders. For a more complete understanding of our business and the Spin-Off, you should read the entire Information Statement carefully, particularly the discussion of “Risk Factors” and the Audited Consolidated Financial Statements and Unaudited Condensed Consolidated Financial Statements and the notes thereto included in the section entitled “Index to Financial Statements.”

We are an independent energy company engaged in the acquisition, development, and production of non-operated oil and natural gas properties in the United States that are generally operated by leading oil companies and are primarily in the Bakken and Three Forks formations in the Williston Basin of North Dakota and Montana. We also have properties in the Central Rockies, including the Denver-Julesburg Basin and the Powder River Basin. Since our inception, we have built a strong and diversified asset base through a combination of property acquisitions, development activities and the implementation of proprietary non-operating platforms and processes utilizing our extensive data resources. We believe the location and concentration of our assets in some of North America’s leading unconventional oil and natural gas resource plays, along with our technical and data capabilities, provide us with acquisition and development opportunities that will result in significant long-term value.

Vitesse has historically created value by acquiring non-operated minority working and mineral interests in oil and natural gas properties, comprising producing wells, near-term development opportunities and undeveloped acreage, and partnering with premier operators with significant experience in developing and producing oil and natural gas in our core areas. Over the past eight years, we have executed on our technical, data driven, and financially disciplined acquisition and development strategy to build our core position in the Williston Basin and Central Rockies and grow our oil and natural gas production. During that time, we have focused on limiting our downside by maintaining conservative acquisition guidelines, limiting our debt leverage and opportunistically hedging our oil production. As a result, we have been able to preserve value when many independent energy companies were forced into financial recapitalizations and restructurings when commodity prices collapsed in 2014, 2018 and 2020.

With the current higher oil and natural gas price environment, we are currently focused on using free cash flow to maintain a strong balance sheet, provide growing returns of capital to stockholders, and grow our oil and natural gas production by developing our extensive inventory of drilling locations and acquiring both producing wells and new development opportunities.

We owned an average working interest of 2.6% in 5,203 gross (133.9 net) productive wells and royalty interests in an additional 998 productive wells as of August 31, 2022. We engage in oil and natural gas well development by participating on a proportionate basis alongside third-party interests in wells drilled and completed in spacing units that include our acreage. As of August 31, 2022, we owned a working interest in 413 gross (8.5 net) wells that were being drilled or completed, and an additional 253 gross (6.5 net) wells that had been permitted for development by our operating partners. We rely on our operators to propose, permit and initiate the drilling and completion of wells. We assess each drilling and completion opportunity on a case-by-case basis and participate in wells that are expected to meet a desired return based upon estimates of recoverable oil and natural gas reserves, anticipated oil and natural gas prices, the expertise of the operator, and the anticipated completed well cost from each project, as well as other factors.

Our non-operated business model provides us with inherent flexibility regarding the cadence of capital deployment and the agility to allocate a portion of our cash flow to the drilling and completion opportunities that we believe will achieve the highest rate of return. We work with more than 35 experienced operators that provide technical insights and opportunities for additional acquisitions and continued development. In

1

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

addition, our business model allows us to not be burdened with various contractual arrangements with respect to minimum drilling obligations, and we can avoid exploratory, upfront leasing and infrastructure costs customarily incurred by operators.

Our operators generally market and sell the oil and natural gas extracted from our wells. In addition, these operators coordinate the transportation of oil and natural gas production from wells in which we participate to appropriate pipelines or rail transport facilities pursuant to arrangements that such operators negotiate and maintain with various parties purchasing such production. The price at which our production is sold generally ties to a market spot price, and the Differential between the market spot price and our realized sales price represents the imbedded transportation and marketing costs of moving the oil and natural gas from the wellhead to the refinery or processing plant. The Differential will fluctuate based on availability of pipeline, rail and other transportation methods.

Vitesse is led by a dedicated management team with extensive experience in the energy industry. Our management team includes Bob Gerrity, our Chief Executive Officer, a successful industry leader who was the founder and chief executive officer of Gerrity Oil & Gas Corporation, which pioneered low-cost “reserve manufacturing” in the Wattenberg field of Colorado during the 1990s. Gerrity Oil & Gas Corporation was one of the most active operators in the United States following its IPO in 1990, at times running more than 15 active drilling rigs and completing as many as 500 wells per year. Gerrity Oil & Gas Corporation merged with Snyder Oil Corporation to form Patina Oil & Gas Corporation in 1996, which was later merged with Noble Energy, Inc. in 2005. Today, these former assets comprise a material portion of Chevron Corporation’s position in the Denver-Julesburg Basin.

Leveraging his prior experience and acknowledging the trend in advances in shale drilling and completion technologies, Mr. Gerrity believed the shale industry would transition to a reserve manufacturing phase marked by well-capitalized and efficient low-cost operators. In 2013, Mr. Gerrity and Brian Cree, our President and Chief Operating Officer, began to seek out non-operated lease and mineral interests with development opportunities in areas of the Williston Basin that were in the core of the field and operated by premier industry leaders, at which time Jefferies Capital Partners made an initial investment in Vitesse Oil to partially fund the acquisition of non-operated working and mineral interests primarily in undeveloped oil and natural gas assets. In 2014, Messrs. Gerrity and Cree began to see a growing number of acquisition and development opportunities in the Williston Basin, and Jefferies made a direct investment in Vitesse to support larger scale acquisition and development efforts. Since that time, Vitesse has completed over 120 acquisitions totaling approximately $520 million and deployed over $400 million in the development of oil and natural gas properties.

Vitesse Oil, which will be acquired by Vitesse as part of the Pre-Spin-Off Transactions, is an independent energy company also engaged in the acquisition, development and production of non-operated oil and natural gas properties in the Williston Basin of North Dakota. As of August 31, 2022, Vitesse Oil had 2,515 net acres in the Williston Basin and owned working interests in approximately 871 gross (7.8 net) productive wells and royalty interests in an additional 120 productive wells, with average production of 816 Boe per day during the month ended August 31, 2022. In addition, Vitesse Oil had 73 gross (0.3 net) wells that were being drilled or completed, and an additional 83 gross (0.3 net) wells that had been permitted for future development by its operators as of August 31, 2022. Based on year-end SEC prices, as of December 31, 2021, Vitesse Oil had approximately 4,107 MBoe of estimated proved reserves located primarily in the core of the Williston Basin, and average production of 641 Boe per day for the year ended December 31, 2021. For information concerning Vitesse Oil, see “Unaudited Pro Forma Condensed Combined Financial Statements.”

Our business strategy is focused on creating long-term stockholder value through the profitable acquisition, development and production of oil and natural gas assets at attractive rates of return, while maintaining a strong

2

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

and conservative balance sheet and distributing a portion of our free cash flow to our stockholders in the form of a regular cash dividend on a quarterly basis. The key elements of our business strategy include the following:

| ∎ | Built to Last. From our inception, we have focused on creating a durable organization that generates strong financial returns and sustainable free cash flow through commodity cycles. As opposed to primarily acquiring producing reserves, we have focused our efforts on acquiring an attractive inventory of undeveloped drilling locations that afford us flexibility in the face of oil and natural gas price fluctuations and have taken advantage of technical improvements and cost reductions over time, supporting the sustainable generation of free cash flow. Our management team fosters a culture of innovation and continuous improvement, constantly looking for ways to improve our operations and technical and data analysis, and strengthen our organizational agility and adaptability. |

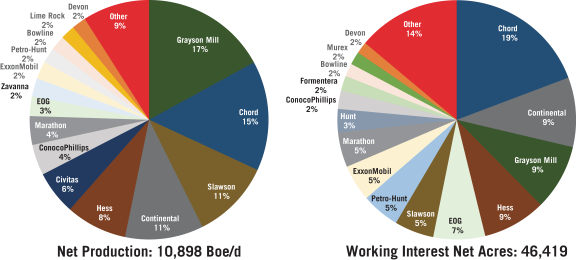

| ∎ | Risk Diversification. We seek to diversify our capital and operational risk through participation in a large number of oil and natural gas wells and with multiple operators across multiple basins. We seek to diversify our risk by operator, formation, value concentration and commodity (oil and natural gas). As of August 31, 2022, we owned an average working interest of 2.6% in 5,203 gross (133.9 net) productive wells and royalty interests in an additional 998 productive wells, with more than 35 experienced operators that provide development and production activities on our oil and natural gas properties. We believe we can further diversify our risk over time with acquisitions in additional basins, focusing on accretive acquisitions of high-quality assets with experienced operators in the most prolific basins in the United States. During the nine months ended August 31, 2022, our average production was 10,048 Boe per day, consisting of approximately 8,910 Boe per day in the Williston Basin and 1,138 Boe per day in the Central Rockies. During the month ended August 31, 2022, our average production was 10,898 Boe per day, consisting of approximately 9,462 Boe per day in the Williston Basin and 1,436 Boe per day in the Central Rockies. |

| ∎ | Growth through Value-Enhancing Acquisitions. We have been a consolidator and clearing house of non-operated working interests in various leading oil and natural gas shale plays in the United States, and we will continue that strategy and potentially pursue operated asset packages and other acquisition strategies going forward. Our near-term drilling acquisition strategy is centered around building a strong presence in our core basins by acquiring smaller non-operated lease and wellbore positions with direct exposure to near-term drilling activity. By virtue of their smaller footprint, these targeted acquisitions have been completed at a significant discount to the prices paid for contiguous acreage positions typically sought by larger producers and operators of oil and natural gas wells. Acquisitions such as these have been a significant driver of increasing our production. Over the last eight years, we have closed approximately 120 discrete acquisitions totaling more than $520 million, and we intend to continue these activities, while at the same time evaluating and pursuing larger asset packages in both our current area of operations and other areas. We believe our disciplined acquisition strategy can responsibly add production, cash flow and scale to existing operations. |

| ∎ | Strong Balance Sheet and Financial Flexibility. We plan for financial strength and flexibility through the prudent management of our balance sheet and free cash flow. During 2020, 2021, and the first nine months of 2022 we were free cash flow positive and reduced our outstanding debt from $104.0 million at November 30, 2019 to $68.0 million at November 30, 2021 and to $66.0 million at August 31, 2022. Following the Spin-Off, we intend to maintain conservative indebtedness and a simple capital structure consisting only of our New Revolving Credit Facility and common stock. We intend to maintain the flexibility to manage our free cash flow by continuing to adhere to a target Net Debt to Adjusted EBITDA ratio (last twelve months) of less than 1.0. As of August 31, 2022, our Net Debt to Adjusted EBITDA ratio (last twelve months) was 0.4. For the twelve months ended August 31, 2022, we generated net income and Adjusted EBITDA of $81.2 million and $158.0 million, respectively. From our inception in 2014 through August 31, 2022, we generated approximately $144.0 million of net income during a volatile commodity price environment. For definitions and reconciliations of Net Debt and Adjusted EBITDA to their most directly comparable financial measures in accordance with GAAP, see “Selected Historical Financial Data—Non-GAAP Financial Information.” |

3

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| ∎ | Dividends to Stockholders. Our business plan focuses on building a diversified, low-leverage, free cash flow generating business that can deliver regular cash dividends to our stockholders. We made cash distributions to our members totaling $25.0 million during 2019, $0.0 during 2020, $12.0 million during 2021, and $42.0 million during the nine months ended August 31, 2022. In addition to the aforementioned cash distribution payments, Jefferies retained close to $25.0 million in hedging gain proceeds that were attributable to derivatives associated with our oil production during 2019 and 2020, further demonstrating our commitment to generating value for our investors. Following the Distribution, we expect that Vitesse will pay quarterly cash dividends totaling approximately $[ ] per fiscal year. |

| ∎ | Hedging Strategy. To reduce our exposure to the volatility of oil prices and protect our ability to pay distributions, we have entered into hedging derivative instruments for a portion of our expected oil production, which have included swaps, collars, puts and other structures. We historically have layered in oil hedges both on an opportunistic basis when WTI prices have allowed us to recognize attractive rates of return on our asset base and upon acquisitions of larger producing assets to protect returns. We currently do not hedge natural gas production due to the mismatch between our operators’ pricing formulas and settlement mechanics on natural gas hedges. Our current hedged position mitigates our exposure to volatile oil prices by layering in hedges covering approximately 30% of our expected oil production through November 30, 2024. However, in the past, based on then-existing market conditions, we have hedged significantly higher percentages of our actual oil production. For further information see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosure about Market Risk—Commodity Price Risk.” |

| ∎ | Responsible Stewards. We are committed to ESG initiatives and seek a culture of improvement in ESG practices. We work to provide safe, reliable and affordable energy in a responsible manner by partnering with responsible operators in our core areas, while being cognizant of the broader energy transition. The key tenets of our ESG philosophy are to identify opportunities to reduce our environmental impact, improve safety, invest in our employees, and support the communities in which we live and work while improving transparency and accountability. At the time of the Distribution, our Board will be majority independent and composed of experienced professionals with a strong background in the energy industry and more broadly in business. |

We believe that we will be able to successfully execute our business strategies because of the following competitive strengths:

| ∎ | Every Decision is a Financial Decision. Our business culture encourages employees to think like owners and to make decisions with a long-term perspective. We have developed a systematic approach of responsibly reviewing acquisition and development opportunities. As part of our efforts to maximize returns, we have established a capital allocation framework with the objective of allocating capital to acquisitions and development of oil and natural gas properties to drive sustainability and growth in free cash flow, the repayment of debt and stockholder dividends. We are focused on a capital allocation framework that entails low development reinvestment rates, allowing us to return a significant portion of our cash flow back to our stockholders, and will retain flexibility with respect to share repurchases, subject to approval from our Board and as conditions warrant. We will continue to evaluate and pursue profitable and accretive acquisition and consolidation opportunities that enhance stockholder value and build scale. As opportunities arise, we intend to identify and acquire additional acreage and producing assets to supplement our existing operations. |

| ∎ | Data and Technology Driven. Our proprietary data-driven approach allows for rapid multi-disciplinary evaluation to determine the most attractive acquisition and development opportunities. We created customized data systems (vLuminis) that are integrated, centralized and utilized by our employees so that decisions are based on a common base of information. We maintain real-time business intelligence dashboards to monitor operators, rigs, well performance, drilling and completion costs and |

4

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| production results. This data informs model forecasts, type curves and decisions about acquisition and development opportunities. We maintain responsive, basin-wide models that are updated in real time and incorporate historical data by operator and region. These models, along with our proprietary systems and platforms, provide necessary inputs and evaluation metrics, which allow us to make informed investment decisions based on forecasted production, operating expenses, type curves, drilling inventory, cash flow and other operational and financial outputs. As a result, we have the capability to process multiple opportunities quickly with the current team in place. |

| ∎ | Experienced Management and Industry Relationships. Vitesse’s management team has developed deep and longstanding relationships with many of our operators, other working interest and mineral owners, investment banks, acquisition and divestiture companies and investors. A majority of our evaluated and executed acquisitions and transactions are self-sourced. We have become a preferred non-operator to some of the largest companies operating in the Williston Basin and Central Rockies given our track record of evaluating and acquiring non-operated oil and natural gas working interests, and being a responsible financial partner. As a result, we see broad deal flow from single wellbore near-term development acquisition opportunities to packages consisting of both producing and undeveloped assets worth hundreds of millions of dollars. Our management team has an over 30-year track record of creating value together at both private and public oil and natural gas companies. |

| ∎ | Proactive Asset Management Philosophy. Our experienced team of landmen and accountants review acquired assets to unlock incremental value. Many assets we acquire have title defects or other land related issues where deep analysis and consistent, quality diligence adds value in many areas, including increased working interest ownership and working capital management. Our long-term view provides the time to solve issues and find additional well interests to increase the velocity of overall returns. This is enabled by strong departmental relationships with operators and accurate data management. |

Industry Trends Impacting Our Business

Commodity prices are the most significant factor impacting our acquisition and divestiture strategy, as well as the decisions of our operators in conducting their operations. Prices for oil and natural gas can be highly volatile. For instance, the COVID-19 pandemic and efforts to mitigate the spread of the disease, combined with OPEC actions in early 2020, led to spot and future prices of oil and natural gas falling to historic lows during the second quarter of 2020 and remaining depressed through much of 2020. Our operators in the Williston Basin responded by significantly decreasing drilling and completion activity, and by shutting in or curtailing production from a significant number of producing wells. Commodity prices, however, quickly reached pre-pandemic levels in the second half of 2021, and during the first nine months of 2022 only further accelerated upward, in part as a result of the Russian invasion of Ukraine. The ongoing conflict between Russia and Ukraine may have further global economic consequences, including disruptions of the global energy markets and the amplification of inflation and supply chain constraints, partially due to sanctions by the European Union, the United Kingdom and the United States on imports of oil and gas from Russia.

As a result of such recent commodity price volatility, which we expect to continue for the remainder of 2022, our earnings and operating cash flows can vary substantially, and are subject to external factors over which the company has no control. While we do hedge a substantial portion of our production, we are still significantly subject to movements in commodity prices. Such volatility can make it difficult to predict future effects on our company and the decisions of our operators. Factors that we expect will continue to impact commodity prices include product demand connected with global economic conditions, industry production and inventory levels, technology advancements, production quotas or other actions imposed by OPEC countries, actions of regulators, and regional supply interruptions or fears thereof that may be caused by military conflicts (including invasion), civil unrest, pandemic or political uncertainty. Any of the foregoing can have a substantial impact on the prices of oil and natural gas, which in turn impacts the decision of our operators to drill and extract resources. Despite such commodity price volatility, we expect that our cash flow from operations and borrowing availability under our Existing Revolving Credit Facility or New Revolving Credit Facility, as applicable, will allow us to meet our liquidity needs for the next twelve months.

5

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

Our principal executive offices are located at 9200 E Mineral Ave, Suite 200, Centennial, Colorado 80112. Our current office space consists of approximately 15,000 square feet of leased space. We believe our current office space is sufficient to meet our needs and that additional office space can be obtained if necessary.

Ownership of Vitesse common stock is subject to numerous risks, including risks relating to the Spin-Off. The following list of risk factors is not exhaustive. Please read the information in the section entitled “Risk Factors” for a more thorough description of these and other risks.

Risks Relating to the Spin-Off

| ∎ | If the Distribution is not a tax-free transaction for U.S. federal income tax purposes, Jefferies and recipients of shares of Vitesse common stock could be subject to significant tax liability, and Vitesse could have an indemnification obligation to Jefferies. |

| ∎ | We intend to agree to numerous restrictions to preserve the non-recognition treatment of the Distribution, which may reduce our strategic and operating flexibility. |

| ∎ | We may be unable to achieve the expected benefits from the Spin-Off, following which we will be subject to new reporting requirements, incur increased costs, and certain members of management and directors may face conflicts of interest. |

| ∎ | Our acquisitions of Vitesse Energy and Vitesse Oil may require consents or approvals, which could harm our business and financial performance if not obtained. |

| ∎ | Until the Distribution occurs, the Jefferies Board may change the terms of the Spin-Off in ways that may be unfavorable to us. |

| ∎ | If you do not want to receive our common stock in the Distribution, your sole recourse will be to divest yourself of your Jefferies common stock. |

Risks Relating to Our Common Stock

| ∎ | No market for our common stock currently exists. Following the Spin-Off, an active trading market may not develop or be sustained, and our stock price may fluctuate significantly. |

| ∎ | Although we expect to pay dividends, we cannot provide assurance that we will pay dividends on our common stock, and our indebtedness may limit our ability to pay dividends on our common stock. |

| ∎ | Certain provisions in our Amended and Restated Certificate of Incorporation, Amended and Restated Bylaws and Delaware law may discourage takeovers. |

| ∎ | The rights associated with our common stock will differ from the rights associated with Jefferies common stock. |

| ∎ | Our Amended and Restated Certificate of Incorporation will designate the Court of Chancery of the State of Delaware as the sole and exclusive forum for certain types of actions and proceedings, potentially limiting our stockholders’ ability to obtain a favorable judicial forum for disputes. |

Risks Relating to Our Business

| ∎ | Our business may be affected by volatile or extended declines in oil and natural gas prices. |

| ∎ | We have incurred net losses in the past, in part due to fluctuations in oil and gas prices, and we may incur such losses again in the future. |

| ∎ | Our estimated proved reserves may prove to be inaccurate. |

| ∎ | Our business relies on third parties, such as our operators, and depends on transportation and processing facilities and other assets that are owned by third parties. |

6

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| ∎ | Seasonal weather conditions may adversely affect our operators’ ability to conduct drilling and completion activities and to sell oil and natural gas for periods of time. |

| ∎ | The majority of our producing properties are located in the Williston Basin, making us vulnerable to risks associated with operating in one major geographic area. |

| ∎ | We may be materially adversely affected by the negative global and economic impact resulting from the military conflict in Ukraine, other geopolitical tensions, ongoing risks from COVID-19, cybersecurity threats, and inflation related costs. |

| ∎ | Asset retirement costs may be difficult to predict and may be substantial. Unplanned costs could divert resources from other projects. |

| ∎ | Increased attention to ESG matters, fuel conservation measures and related governmental initiatives, technological advances and negative shift in market perception towards the oil and natural gas industry could reduce demand for oil and natural gas. |

Risks Relating to Our Indebtedness

| ∎ | Any significant reduction in our borrowing base under our New Revolving Credit Facility may negatively impact our financial results or restrict our business and financing activities. |

| ∎ | We may not be able to generate enough cash flow to meet our current or potential future debt obligations or to pay dividends to our stockholders. |

| ∎ | Variable rate indebtedness could subject us to interest rate risk, which could cause our debt service obligations to increase significantly. |

| ∎ | Our business plan requires the expenditure of significant capital, which we may be unable to obtain on favorable terms or at all. |

Risks Relating to Legal and Regulatory Matters

| ∎ | New federal rules and regulations could restrict our ability to acquire federal leases and/or impose more onerous permitting and other costly environmental, health and safety requirements. |

| ∎ | Certain U.S. federal income tax deductions currently available with respect to oil and natural gas development may be eliminated as a result of future legislation. |

| ∎ | Legislative and regulatory developments could have an adverse effect on our ability to use derivative instruments to reduce the effect of volatile oil and natural gas price, interest rate and other risks associated with our business. |

| ∎ | Our business is subject to complex federal, state, and local laws, as well as other laws and regulations that could adversely affect the cost, manner or feasibility of doing business. |

| ∎ | Federal and state legislative and regulatory initiatives relating to climate change, hydraulic fracturing and reducing gas flaring could result in increased costs and additional operating restrictions or delays. |

We expect the following transactions, among others, to be consummated prior to the completion of the Spin-Off (which we refer to as the “Pre-Spin-Off Transactions”):

| ∎ | Vitesse was incorporated on August 5, 2022; |

| ∎ | 3B Energy will transfer all of its Vitesse Energy equity interests to Vitesse Energy Finance as repayment for prior loans from Vitesse Energy Finance to 3B Energy; |

| ∎ | Each of Messrs. Gerrity and Cree will transfer all of their vested Vitesse Energy MIUs to Vitesse Energy Finance as repayment for prior loans from Vitesse Energy Finance to each of Messrs. Gerrity and Cree; |

| ∎ | Vitesse Energy Finance and the remaining holders of vested Vitesse Energy MIUs will transfer all of their Vitesse Energy equity interests to Vitesse in exchange for newly issued shares of Vitesse common stock; |

| ∎ | Jefferies Capital Partners, Gerrity Bakken and holders of vested Vitesse Oil MIUs will transfer all of their Vitesse Oil equity interests to Vitesse in exchange for newly issued shares of Vitesse common stock; |

7

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| ∎ | Through a series of distributions, all of the Vitesse common stock held by Vitesse Energy Finance will ultimately become held directly by Jefferies; |

| ∎ | Through a series of distributions, a portion of the Vitesse common stock held by Jefferies Capital Partners will ultimately become held directly by Jefferies; and |

| ∎ | Vitesse will enter into the New Revolving Credit Facility and will use a portion of the proceeds from borrowings under the New Revolving Credit Facility to repay in full and terminate the Existing Revolving Credit Facility and to repay in full and terminate the Vitesse Oil Revolving Credit Facility. |

Pursuant to the above described transactions, Jefferies will directly hold approximately [ ]% of the total issued and outstanding common stock of Vitesse immediately prior to the Distribution. For more information, see “The Spin-Off—Pre-Spin-Off Transactions” and “Certain Relationships and Related Party Transactions—Other Transactions and Relationships with Related Persons.”

On July 19, 2022, Jefferies announced plans for the complete legal and structural separation of Vitesse from Jefferies.

To effect the separation, first, Jefferies and Jefferies Capital Partners, among others, will undertake the Pre-Spin-Off Transactions described under the section entitled “The Spin-Off—Pre-Spin-Off Transactions.” Jefferies will subsequently distribute all of Vitesse’s outstanding common stock held by Jefferies, representing [ ]% of our total issued and outstanding common stock immediately prior to the Distribution, to Jefferies shareholders, and Vitesse will become an independent, publicly traded company. After the Distribution, Jefferies will not own any shares of our common stock.

Prior to completion of the Spin-Off, we intend to enter into a Separation and Distribution Agreement and a Tax Matters Agreement with Jefferies related to the Spin-Off. These agreements will govern the relationship between Jefferies and us up to and after completion of the Spin-Off. See the section entitled “Certain Relationships and Related Party Transactions” for more detail. No approval of Jefferies shareholders is required in connection with the Spin-Off, and Jefferies shareholders will not have any appraisal rights in connection with the Spin-Off.

Completion of the Spin-Off is subject to the satisfaction, or the waiver by the Jefferies Board, of a number of conditions. If the Jefferies Board waives any condition prior to the effectiveness of the Registration Statement on Form 10, of which this Information Statement is a part, and the result of such waiver is material to Jefferies shareholders, Jefferies will file an amendment to the Registration Statement to revise the disclosure in this Information Statement accordingly. In the event that the Jefferies Board waives a condition after this Registration Statement becomes effective and such waiver is material to Jefferies shareholders, Jefferies will communicate such change to Jefferies shareholders by filing a Current Report on Form 8-K describing the change.

In addition, Jefferies has the right not to complete the Spin-Off if, at any time, the Jefferies Board determines, in its sole and absolute discretion, that the Spin-Off is not in the best interests of Jefferies or its shareholders, or is otherwise not advisable. If the Spin-Off is not completed for any reason, Jefferies and Vitesse will have incurred significant costs related to the Spin-Off, including fees for consultants, financial and legal advisors, accountants and auditors, that will not be recouped. Total one-time transaction costs associated with the Spin-Off are preliminarily estimated to range from $[ ] to $[ ] if the Spin-Off is completed. If the Spin-Off is not completed for any reason, the one-time transaction costs will generally be limited to the transaction costs incurred for services rendered as of the date the Spin-Off is abandoned, which will be less than the ranges noted above. Our management has devoted significant time to manage the Spin-Off process, which has decreased the time they have had to manage the business of Vitesse. See the section entitled “The Spin-Off—Conditions to the Spin-Off” for more detail.

8

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

In 2017, Jefferies announced that its primary business initiative would be to become a focused financial services company with clear drive and direction, concentrating on investment banking and capital markets and alternative asset management. Since that time, Jefferies has strategically and opportunistically monetized a significant portion of its merchant banking portfolio and realigned its internal structure to achieve those goals. Jefferies has continued to make clear that it would continue to liquidate its merchant banking portfolio, with the intention of selling the businesses and investments comprising the portfolio to third parties, distributing the businesses and investments comprising the portfolio to shareholders or transferring the balance of the businesses and investments comprising the portfolio to its asset management reportable segment. As they contemplated the Spin-Off, the Jefferies Board and management determined that positioning Vitesse as an independent publicly traded company would further Jefferies’ long-term goals and enhance stockholder value.

A wide variety of factors were considered by the Jefferies Board in evaluating the Spin-Off. Among other things, the Jefferies Board considered several potential benefits of the Spin-Off, including:

| ∎ | Strategic goals. Following the Spin-Off, Jefferies will be one step closer to its previously announced goal of liquidating its merchant banking portfolio and focusing solely on financial services. |

| ∎ | Maximizing shareholder value and choice. Jefferies shareholders should benefit from both the benefits to be reaped as Jefferies further reduces its merchant banking portfolio and further dedicates its management’s focus on financial services and from the potential for value enhancement that might be achieved in a stand-alone, publicly traded Vitesse. Jefferies believes the Spin-Off will help unlock the value in Vitesse that may not be clear to investors while it remains part of Jefferies. Those investors looking for a pure play company that is focused on creating long-term stockholder value through the profitable acquisition, development and production of oil and natural gas assets will be able to invest directly in Vitesse, which should result in greater alignment between the interests of each company’s stockholder base and the characteristics of its respective business, capital structure and financial results. |

| ∎ | Separate capital structures and allocation flexibility. The Spin-Off will enable each of Jefferies and Vitesse to leverage its distinct profile and cash flow characteristics to optimize its capital structure and capital allocation strategy. The Spin-Off will permit each company to allocate its financial resources to meet the unique needs of its own businesses, which will allow each company to intensify its focus on its distinct strategic priorities and individual business risk and return profiles. |

The Jefferies Board also considered several potentially negative factors in evaluating the Spin-Off. Notwithstanding these negative factors, the anticipated effects of which are not reasonably determinable, and considering the factors discussed above, the Jefferies Board determined that the Spin-Off provided the best opportunity to achieve the above benefits and enhance stockholder value. Neither Jefferies nor Vitesse can assure you that, following the Spin-Off, any of the benefits described above or otherwise will be realized to the extent anticipated or at all. For additional information, see the sections entitled “Risk Factors” and “The Spin-Off—Reasons for the Spin-Off.”

Emerging Growth Company Status

We are an “emerging growth company” as defined by the Jumpstart Our Business Startups Act of 2012. We will continue to be an emerging growth company until the earliest to occur of the following:

| ∎ | the last day of the fiscal year in which our total annual gross revenues first meet or exceed $1.235 billion (as adjusted for inflation); |

| ∎ | the date on which we have, during the prior three-year period, issued more than $1.0 billion in non-convertible debt; |

| ∎ | the last day of the fiscal year in which we (1) have an aggregate worldwide market value of common stock held by non-affiliates of $700 million or more (measured at the end of each fiscal year) as of the |

9

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| last business day of our most recently completed second fiscal quarter and (2) have been a reporting company under the Exchange Act for at least one year (and filed at least one annual report under the Exchange Act); or |

| ∎ | the last day of the fiscal year following the fifth anniversary of the date of the first sale of our common stock pursuant to an effective registration statement under the Securities Act. |

For as long as we are an emerging growth company, we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements in the assessment of our internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act of 2002, exemption from new or revised financial accounting standards applicable to public companies until such standards are also applicable to private companies, reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements, and exemptions from the requirement of holding a nonbinding advisory vote on executive compensation and stockholder approval on golden parachute compensation not previously approved. We may choose to take advantage of some or all of these reduced burdens. For example, we have taken advantage of the reduced disclosure obligations regarding executive compensation in this Information Statement. For as long as we take advantage of the reduced reporting obligations, the information we provide stockholders may be different from information provided by other public companies. In addition, it is possible that some investors will find our common stock less attractive as a result of these elections, which may result in a less active trading market for our common stock and higher volatility in our stock price.

In addition, we intend to take advantage of the extended transition period that allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. Our election to use the extended transition period permitted by this election may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the extended transition period and who will comply with new or revised financial accounting standards.

Vitesse Energy has a secured Existing Revolving Credit Facility with Wells Fargo Bank, N.A., as administrative agent, and a syndicate of banks, as lenders. The Existing Revolving Credit Facility will mature on April 29, 2026. The Existing Revolving Credit Facility permits borrowing on a revolving credit basis with availability equal to the least of (1) the current aggregate elected commitments of $170 million, (2) the current borrowing base of $200 million and (3) the maximum credit amount of $500 million. The aggregate elected commitments of the lenders under the Existing Revolving Credit Facility may be increased up to a maximum credit amount of $500 million, subject to the satisfaction of certain customary conditions, including the willingness of the existing lenders to increase their commitments or of new lenders to provide additional commitments. In connection with the closing of the Existing Revolving Credit Facility in April 2022, the borrowing base was set at $200 million. Our borrowing base under the Existing Revolving Credit Facility is subject to regular, semi-annual redeterminations on or about April 1 and October 1 of each year based on, among other things, the value of our proved oil and natural gas reserves, as determined by the lenders in their discretion. As of August 31, 2022, under the Existing Revolving Credit Facility we had outstanding borrowings of $66.0 million and $104.0 million of available borrowing capacity. At our option, borrowings under the Existing Revolving Credit Facility bear interest at either an adjusted forward-looking term rate based on SOFR (“Term SOFR”) or an adjusted base rate (“Base Rate”) (the highest of the administrative agent’s prime rate, the federal funds rate plus 0.50% or the 30-day Term SOFR rate plus 1.0%), plus an applicable margin ranging from 1.75% to 2.75% with respect to Base Rate borrowings and 2.75% to 3.75% with respect to Term SOFR borrowings, in each case based on the current commitment utilization percentage. The Existing Revolving Credit Facility is guaranteed by all of our subsidiaries and is collateralized by a first priority lien on substantially all assets of Vitesse Energy and its subsidiaries, including a first priority lien on properties representing a minimum of 85% of the proved reserve value of our oil and natural gas properties.

Vitesse intends to enter into a secured New Revolving Credit Facility in connection with the Spin-Off. The New Revolving Credit Facility will replace the Existing Revolving Credit Facility of Vitesse Energy. As the terms of

10

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

the credit agreement governing the New Revolving Credit Facility are finalized, we will provide the required and appropriate information in subsequent amendments to the Registration Statement on Form 10, of which this Information Statement is a part.

We are a Delaware corporation. Our principal executive offices are located at 9200 E. Mineral Ave. Suite 200, Centennial, Colorado 80112. Our telephone number is (720) 361-2500. Our website address is www.[ ].com. Information contained on, or connected to, our website or Jefferies’ website does not and will not constitute part of this Information Statement or the Registration Statement on Form 10, of which this Information Statement is a part, or any other filings with, or any information furnished or submitted to, the SEC.

Reasons for Furnishing This Information Statement

We are furnishing this Information Statement solely to provide information to Jefferies shareholders who will receive shares of our common stock in the Distribution. Jefferies shareholders are not required to vote on the Distribution. Therefore, you are not being asked for a proxy and you are not required to send a proxy to Jefferies. You do not need to pay any consideration, exchange or surrender your existing shares of Jefferies common stock or take any other action to receive your shares of Vitesse common stock. You should not construe this Information Statement as an inducement or encouragement to buy, hold or sell any of our securities or any securities of Jefferies. We believe that the information contained in this Information Statement is accurate as of the date set forth on the cover. Changes to the information contained in this Information Statement may occur after that date, and neither we nor Jefferies undertakes any obligation to update the information except in the normal course of our and Jefferies’ respective public disclosure obligations and practices.

11

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

QUESTIONS AND ANSWERS ABOUT THE SPIN-OFF

The following provides only a summary of certain information regarding the Spin-Off. You should read this Information Statement in its entirety for a more detailed description of the matters described below.

| Q: | Why am I receiving this Information Statement? |

| A: | Jefferies is making this Information Statement available to you because you are a holder of shares of Jefferies common stock. If you are a holder of shares of Jefferies common stock as of the Record Date, for every [ ] shares of Jefferies common stock that you hold as of the Record Date, you will be entitled to receive [ ] shares of Vitesse common stock. This Information Statement will help you understand how the Spin-Off will affect your post-Distribution ownership in Jefferies and Vitesse. |

| Q: | What is the Spin-Off? |

| A: | The Spin-Off is the method by which we will separate from Jefferies. In the Spin-Off, Jefferies will distribute to its shareholders all the outstanding shares of our common stock held by Jefferies, which we refer to as the “Distribution.” Following the Spin-Off, we will be an independent, publicly traded company, and Jefferies will not retain any ownership interest in us. Jefferies will continue as an independent, publicly traded company primarily focused on its investment banking and capital markets and asset management businesses. |

| Q: | Will the number of Jefferies shares I own change as a result of the Spin-Off? |

| A: | No, the number of shares of Jefferies common stock you own will not change as a result of the Spin-Off. |

| Q: | What are the reasons for the Spin-Off? |

| A: | A wide variety of factors were considered by the Jefferies Board in evaluating the Spin-Off. Among other things, the Jefferies Board considered several potential benefits of the Spin-Off, including: |

| ∎ | Strategic goals. Following the Spin-Off, Jefferies will be one step closer to its previously announced goal of liquidating its merchant banking portfolio and focusing solely on financial services. |

| ∎ | Maximizing shareholder value and choice. Jefferies shareholders should benefit from both the benefits to be reaped as Jefferies further reduces its merchant banking portfolio and further dedicates its management’s focus on financial services and from the potential for value enhancement that might be achieved in a stand-alone, publicly traded Vitesse. Jefferies believes the Spin-Off will help unlock the value in Vitesse that may not be clear to investors while it remains part of Jefferies. Those investors looking for a pure play company that is focused on creating long-term stockholder value through profitable acquisition, development and production of oil and natural gas assets will be able to invest directly in Vitesse, which should result in greater alignment between the interests of each company’s stockholder base and the characteristics of its respective business, capital structure and financial results. |

| ∎ | Separate capital structures and allocation flexibility. The Spin-Off will enable each of Jefferies and Vitesse to leverage its distinct profile and cash flow characteristics to optimize its capital structure and capital allocation strategy. The Spin-Off will permit each company to allocate its financial resources to meet the unique needs of its own businesses, which will allow each company to intensify its focus on its distinct strategic priorities and individual business risk and return profiles. |

The Jefferies Board also considered several potentially negative factors in evaluating the Spin-Off. Notwithstanding these negative factors, the anticipated effects of which are not reasonably determinable, and considering the factors discussed above, the Jefferies Board determined that the Spin-Off provided the best opportunity to achieve the above benefits and enhance stockholder value. Neither Jefferies nor Vitesse can assure you that, following the Spin-Off, any of the benefits described above or otherwise will be realized to the extent anticipated or at all. For additional information, see the sections entitled “Risk Factors” and “The Spin-Off—Reasons for the Spin-Off.”

12

Confidential Treatment Requested by Vitesse Energy, Inc.

Pursuant to 17 C.F.R. Section 200.83

| Q: | Why is the separation of Vitesse structured as a spin-off? |

| A: | Jefferies believes that a distribution of our shares to holders of Jefferies common stock, which Jefferies intends to be tax-free for U.S. federal income tax purposes, is the most efficient way to separate our business from Jefferies in a manner that will achieve the above benefits. |

| Q: | What will I receive in the Distribution in respect of my shares of Jefferies common stock? |